How economic pressures can impact digital lending today

By Danielle Sesko, Director, Product Management TruStage™

Lending is the lifeblood of the economy, facilitating investments, consumption and economic growth. However, lending activities are inherently tied to the prevailing economic conditions, with shifts in economic indicators impacting borrower behavior, creditworthiness and lender risk appetite. Economic pressures, ranging from inflation and interest rates to unemployment and GDP growth, exert profound effects on lending markets, influencing both the supply and demand sides of the lending equation.

The relationship between wage growth and inflation

Wage growth is another key factor influencing the ability of individuals to repay loans. Nearly 58% of respondents to our survey said they were either somewhat or very concerned that unexpected expenses may come up, which would affect their ability to repay a loan.¹ Digital lenders rely on accurate assessments of borrowers' financial capabilities, and stagnant or declining wages can pose challenges. Changes in income levels can affect the overall creditworthiness of potential borrowers, influencing the risk profile of digital lending portfolios.

To adapt to fluctuations in wage growth, digital lenders should employ sophisticated algorithms and risk management practices to ensure responsible lending. Adjusting traditional credit scoring models and loan terms helps these platforms strike a balance between risk mitigation and providing access to credit for a broader segment of the population. In fact, more consumers today say they are likely to look at different term lengths (28% in 2023 vs. 19% in 2019) and different types of loans (16% in 2023 vs. 12% in 2019) than what they were originally considering.¹

The rapid increase in wage growth following the end of the pandemic caused unusual inflation shocks. This is relevant for lenders, as their cost of funds will fluctuate while the Federal Reserve navigates inflation. Wages are still catching up with inflation rate changes following the pandemic, indicating that there's potential for wage growth to surpass inflation without generating extra price pressures.

Shifting lending capital dynamics

In the evolving realm of capital markets, 2024 presents promising indications of heightened activity, creating ample opportunities for lenders to broaden their lending portfolios.

High-yield bonds and leveraged loans: Seizing mergers and acquisitions (M&A) prospects

The growing investor confidence in high-yield bonds and speculative-grade loans indicates a favorable environment for lenders. The resilience of investment-grade corporate bond markets amidst evolving economic conditions is noteworthy. Gross issuance in 2024 is expected to reach $1.3 trillion in 2024 compared with $1.2 trillion in 2023, but net new issuance after maturities, calls, tenders and bond repurchases is expected at only $475 billion, lower than last year's amount of nearly $500 billion.²

Lenders can leverage this trend by facilitating refinancing and financing for acquisitions, capitalizing on the allure of high yields on cash. Furthermore, new capital regulations may spur additional offerings from the financial sector, providing lenders with avenues to expand their lending activities.

Strategic considerations for lenders

As lenders navigate the shifting landscape of capital markets in 2024, strategic considerations emerge.

- Diversification: Explore opportunities across various market segments, including equity capital markets, high-yield bonds, leveraged loans and investment-grade corporate bonds, to diversify lending portfolios and mitigate risks.

- Timeliness: Stay informed on market dynamics and expedite financing for initial public offerings (IPOs), M&A transactions and bond issuances to capitalize on favorable conditions and meet borrower demand effectively.

When considering the above strategic approaches, it’s good to know what trends are driving demand.

Trends impacting consumer credit demand

Consider these trends influencing consumer credit demand in the marketplace. Across a few categories, demand is decreasing as Americans find it harder to cope with higher prices and levels of debt.

- The Federal Reserve’s increase in short-term interest rates has slowed consumer credit demand nationwide, especially auto lending. In response, captive auto lenders have become more competitive and lowered their interest rates aggressively. This has reduced credit union and bank indirect lending opportunities.

- To keep loan balances growing, some lenders are reaching further down the credit tiers, accepting more subprime and near-prime borrowers than before.

- Rising home prices have increased homeowners' home equity and, therefore, their demand for home equity loans, which is currently one of the fastest loan growth categories.

- Above trend inflation has increased credit card loan balances as low- and middle-income Americans find it hard to make ends meet. They rely on consumer credit to maintain spending patterns in the hope future wage growth will help them pay back their debt later.

- Higher debt levels, the resumption of student loan payments and tighter restrictions on welfare eligibility have led to deteriorating credit quality as loan delinquency and loan charge-off rates increased during the last year.

The need for easier access to credit has helped alternative lending solutions grow, spurring a new challenge and opportunity for competing digital lenders.

The rise of alternative lending solutions

Alternative lending solutions pose both a challenge and an opportunity for digital lenders. As the financial landscape continues to mature, traditional and non-traditional players enter the market, offering innovative lending solutions. Peer-to-peer lending, buy now pay later (BNPL), crowdfunding and decentralized finance (DeFi) platforms are gaining traction as alternatives to traditional digital lending models.

Alternative lending solutions can step in where conventional financial institutions may hesitate, offering accessible financial avenues for consumers with limited or no credit history, lower incomes or non-traditional employment. Some alternative lenders could assess creditworthiness beyond traditional metrics, considering a broader range of factors such as billing transaction history, online behavior and even educational background. This inclusive approach enables these lenders to extend credit to individuals who may have been overlooked and underserved by traditional institutions.

To stay competitive, digital lenders must keep a pulse on emerging technologies and explore partnerships or integrations with alternative lending solutions.

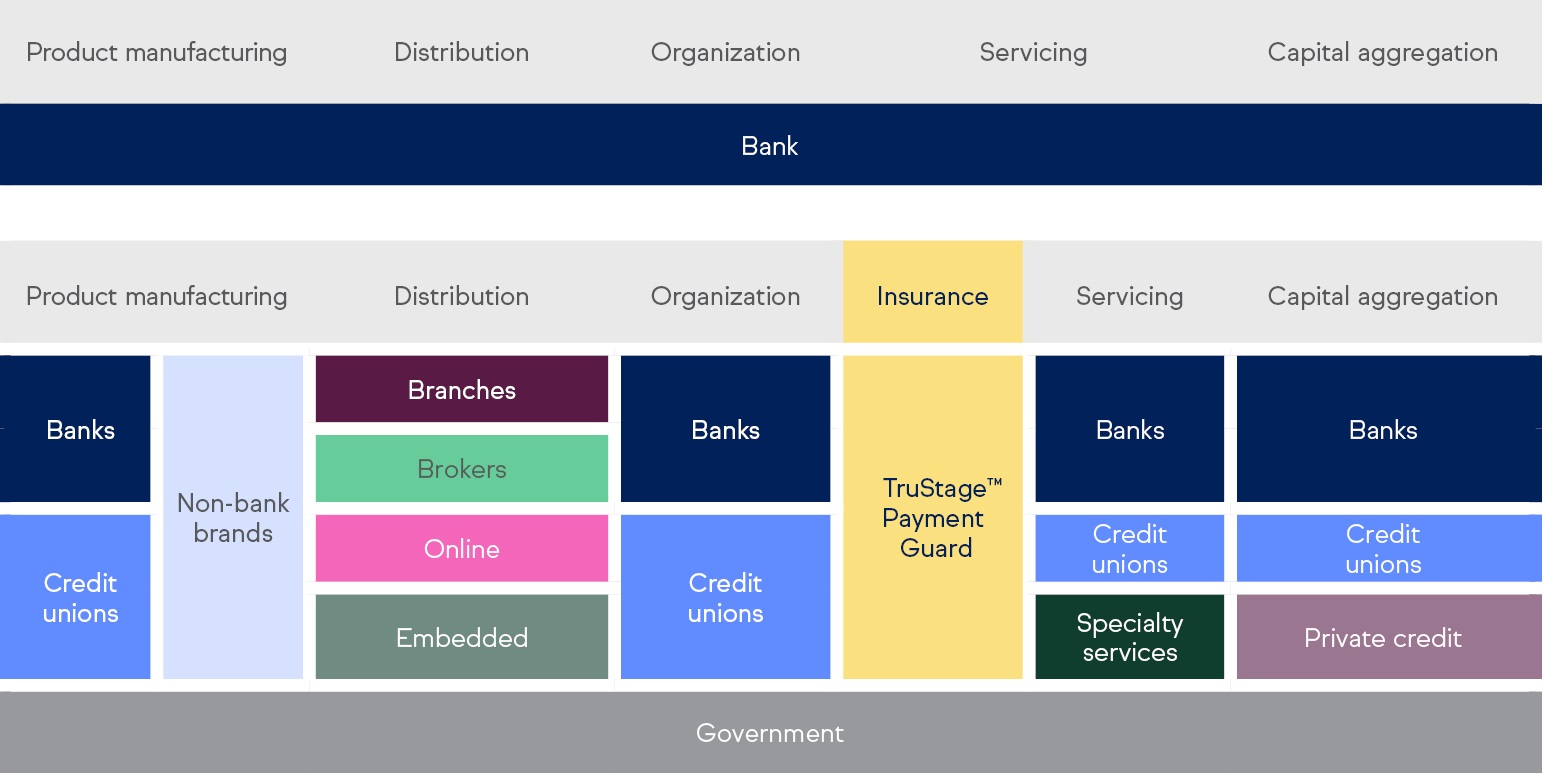

The missing puzzle piece: digital lending insurance

Digital lending insurance (DLI) stands out as the missing piece that completes the consumer lending value chain puzzle. The absence of a robust insurance strategy tailored for digital lending creates a significant gap in the overall value proposition. Introducing DLI products, like TruStage™ Payment Guard Insurance, addresses the vulnerabilities that borrowers may face, providing them with a safety net against unforeseen circumstances such as job loss, disability or other life events that could impact their ability to repay loans.

By integrating Payment Guard Insurance as seamlessly as possible into the consumer lending value chain, digital lenders can enhance the resilience of the lending ecosystem, helping ensure a more sustainable and secure environment for both borrowers and lenders alike. This comes at an important time in our country when economic turbulence has borrowers across the nation concerned about their ability to repay their loans.

Digital lenders operate in a dynamic digital environment that's constantly being reshaped by economic pressures. Finding solutions that can be flexible and easily integrated into current workflows requires a combination of adaptability, data-driven decision-making and a commitment to maintaining trust with consumers.

To learn more about digital lending insurance products like Payment Guard, contact us by following the link.

Want to learn more?

Learn more about embedded insurance and loan payment protection products at TruStage Payment Guard Insurance.